Should You Wait for Rates to Drop More — or Buy Now in DC?

February 20, 2026

February 20, 2026

Should You Wait for Rates to Drop More — or Buy Now in DC?

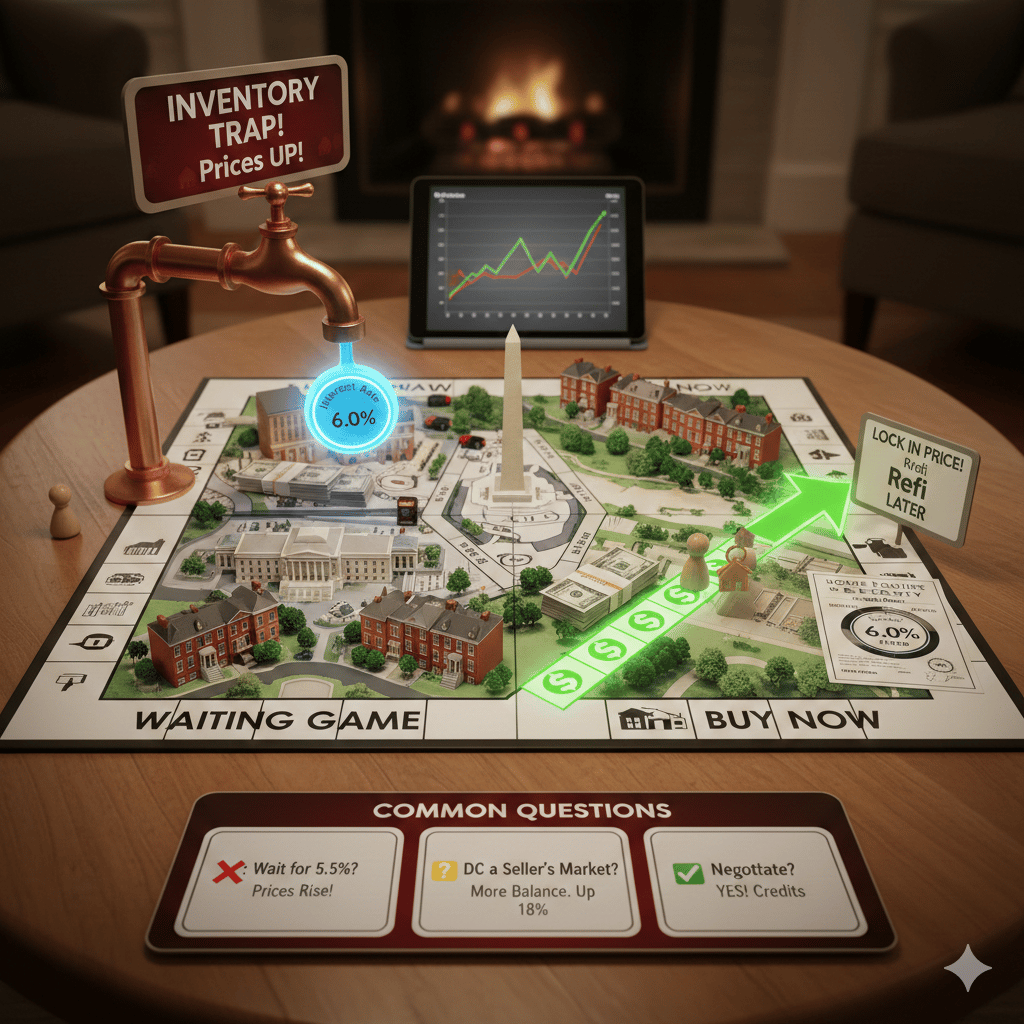

In the D.C. metro area, the "waiting game" has become a local pastime. With mortgage rates finally easing from their 2025 peaks to around 6.0% this February, many prospective buyers are hovering over the "search" button, wondering if holding out for a dip into the 5s is the savvy move. But in a market as historically tight as the DMV (D.C., Maryland, Virginia), timing the market often matters less than "time in" the market.

Appreciation Trends in the DMV

Despite the national narrative of a "housing cooldown," D.C. remains a high-demand island. As of February 2026, the median sold price in the District reached $652,500, an 18% jump over the previous year. While some surrounding areas like Prince George’s County have seen slight dips, the inner core—especially single-family homes in neighborhoods like Arlington and NW D.C.—continues to climb.

If you wait 12 months for a minor rate drop, you may find that the home you wanted now costs significantly more. In the DMV, price appreciation frequently outpaces the savings generated by a slightly lower interest rate.

Rent vs. Own Comparison

The "cost of waiting" isn't just about purchase prices; it’s about the rent you’re paying in the meantime. While D.C. rents have seen a slight 1.9% dip to an average of $2,467, they remain among the highest in the nation.

Every month spent renting is a month of 0% return. While your mortgage payment might be higher initially, it acts as a "forced savings account" through equity. Many savvy D.C. buyers are choosing to "marry the house and date the rate"—buying now to lock in today’s price and planning to refinance if rates hit the 5% mark later this year.

Inventory Risk: The "Floodgate" Effect

The biggest danger of waiting is the inventory trap. Currently, active listings in the D.C. metro are up about 18%, giving buyers rare breathing room and negotiating power.

The moment rates drop significantly, thousands of "sidelined" buyers will likely rush back into the market. This surge in demand typically triggers:

Common Questions & Answers

Q: Is it better to wait for rates to hit 5.5%? A: Waiting for a 0.5% drop might save you a few hundred dollars a month, but if home prices rise by even 3% in that time, your required down payment and total loan amount increase, often wiping out the interest savings.

Q: Is D.C. still a "Seller's Market" in 2026? A: It is becoming more balanced. With inventory up 18%, buyers have more leverage today than they have had in years. However, high-quality listings in popular neighborhoods still move fast.

Q: Can I still negotiate with sellers? A: Yes. Unlike the pandemic-era frenzy, 2026 buyers are successfully negotiating for seller credits to buy down their interest rates or cover closing costs.

For more deep dives into neighborhood trends, mortgage strategies, and D.C. real estate news, visit our blog at cruzregroup.com/blog.

Experience personalized real estate service with Team Cruz, a determined and passionate professional group. With a background in finance and a commitment to creating generational wealth, they provide a white-glove experience, anticipating your needs and exceeding expectations. Discover your dream home with a team that values relationships and delivers results.