Selling Your Home Before Leaving the U.S.: Where Do You Start?

April 24, 2026

April 24, 2026

Relocating from the DC Metro area—whether you are finishing a diplomatic posting in Fairfax or heading home from the biotech hubs of Bethesda and Loudoun—requires a precise exit strategy. Unlike a local move, selling your U.S. home as international staff involves unique tax and legal hurdles.

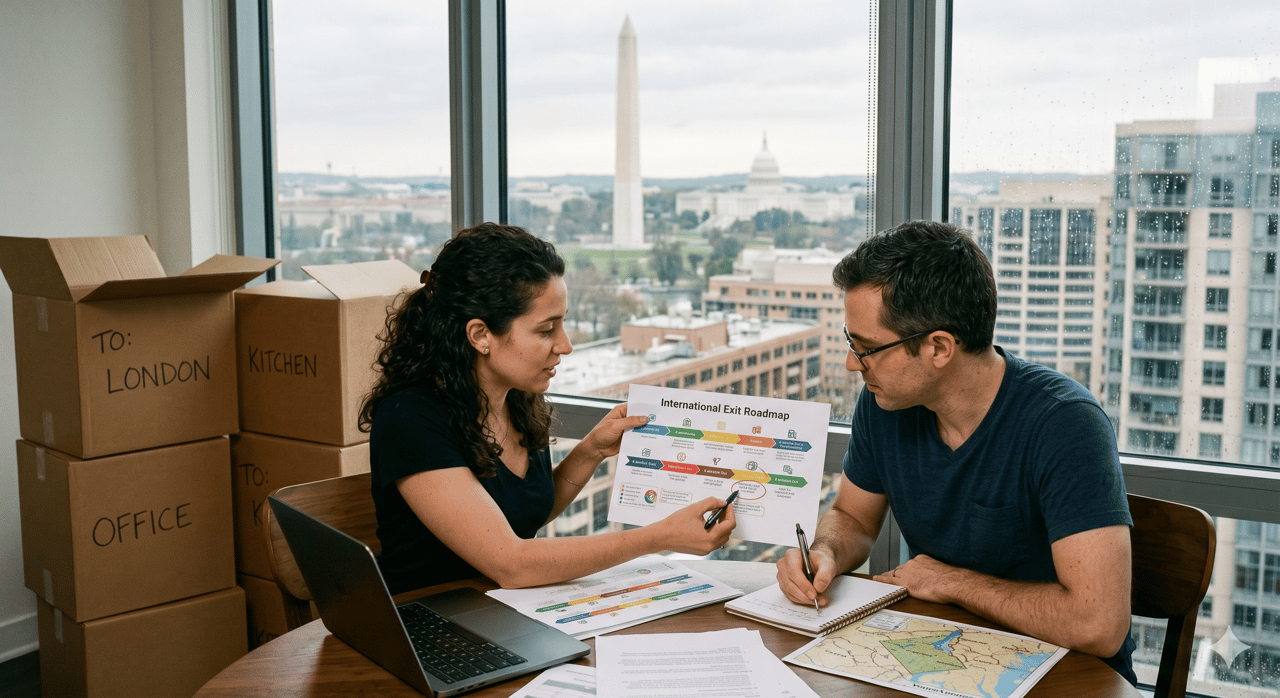

6 Months Out: Consult a tax professional regarding FIRPTA (Foreign Investment in Real Property Tax Act).

4 Months Out: Interview local agents familiar with international sales.

2 Months Out: List your home. The DMV market moves fast, but document authentication for overseas sellers can add weeks.

1 Month Out: Power of Attorney. If you’re leaving before closing, appoint a local representative to sign final papers.

“Selling Your Home Before Leaving the U.S.: Where Do You Start?”

A: Your first move is determining your tax status. For most international staff, the IRS requires a 15% withholding of the gross sales price at closing under FIRPTA. Start by applying for an ITIN if you don’t have an SSN and filing for a Withholding Certificate (Form 8288-B) if you believe your actual tax liability is lower than 15%. Doing this early prevents your equity from being "frozen" by the IRS for months after you've left the country.

Experience personalized real estate service with Team Cruz, a determined and passionate professional group. With a background in finance and a commitment to creating generational wealth, they provide a white-glove experience, anticipating your needs and exceeding expectations. Discover your dream home with a team that values relationships and delivers results.