How Builder Rate Buydowns Work — And Why They Matter

March 12, 2026

March 12, 2026

How Builder Rate Buydowns Work — And Why They Matter

With interest rates staying center stage in the housing market, "Builder Rate Buydowns" have become a secret weapon for buyers. Essentially, a builder pays an upfront fee to the lender to lower your mortgage interest rate, either temporarily or for the life of the loan. It’s a win-win: the builder sells the home, and you get a much more manageable monthly payment.

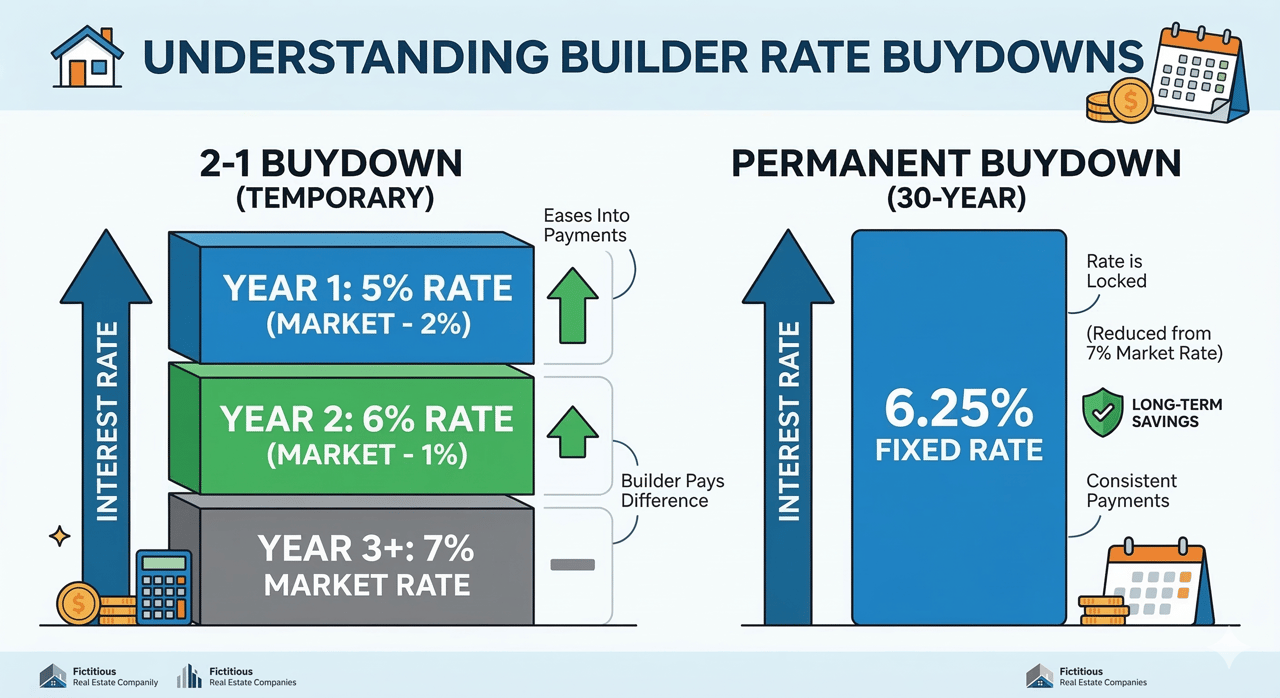

The Two Main Flavors

Real-World Impact

Imagine a $400,000 loan at a 7% market rate.

Q&A Section

Q: Is a buydown better than a price reduction? A: Often, yes. A $10,000 price cut might only save you $60 a month, whereas $10,000 applied to a rate buydown could save you hundreds per month.

Q: What happens if I refinance during a 2-1 buydown? A: If you refinance before the temporary period ends, the remaining "subsidy" funds paid by the builder are typically applied to your principal balance.

Q: Do I have to qualify at the lower rate? A: No. Lenders usually require you to qualify at the "note rate" (the full interest rate) to ensure you can still afford the home once the discount period ends.

Follow for more at https://cruzregroup.com/blog

Experience personalized real estate service with Team Cruz, a determined and passionate professional group. With a background in finance and a commitment to creating generational wealth, they provide a white-glove experience, anticipating your needs and exceeding expectations. Discover your dream home with a team that values relationships and delivers results.